The MLP: How We Decide Which Markets Are Leverageable

Every market on Ultramarkets goes through a formal risk evaluation before listing. This is the full breakdown: gap risk, temporal arbitrage, liquidity depth, resolution certainty, and why saying no to most markets is the most important decision we make.

If you're trading on Ultramarkets right now, you've probably noticed that some of the most viral Polymarket markets never show up on our platform. You might have wondered why.

If you're thinking of LPing once our vault goes public, you should be wondering why — because the answer to that question is the same answer to "why should I trust this protocol with my capital?"

This piece explains the thinking. Not marketing language. The actual risk logic behind why we say no to most markets, what an MLP is, and what a market has to look like before we say yes.

Why This Is Unique to Prediction Markets

When you trade BTC-USD on a perpetual futures platform, the price moves continuously. Your position can be liquidated at any point along a smooth curve. There's always a next price tick, always a functioning order book, always a window to exit.

Prediction markets break this completely.

Every prediction market is hurtling toward a binary collision with reality. "Will the Fed hold rates in April?" trades at 65¢ today, 93¢ tomorrow — and on the day of the FOMC announcement, it resolves to exactly $1.00 or $0.00. Not $0.95. Not $0.87. Exactly one or zero.

Now imagine you're 10x leveraged long at 90¢. The event resolves "No." Your position doesn't slide from 90¢ to 85¢ to 70¢ — it gaps from 90¢ to 0¢ instantaneously. Your collateral is gone. The vault's capital is gone. The liquidation engine never had a chance to fire.

This is gap risk — a fundamental incompatibility between binary resolution and borrowed capital. It's why Polymarket caps at 1x, and why every previous attempt to build leveraged prediction markets has either failed or never launched.

How We Solve This And Why It Creates the Listing Problem

We don't try to survive the gap. We exit before it arrives.

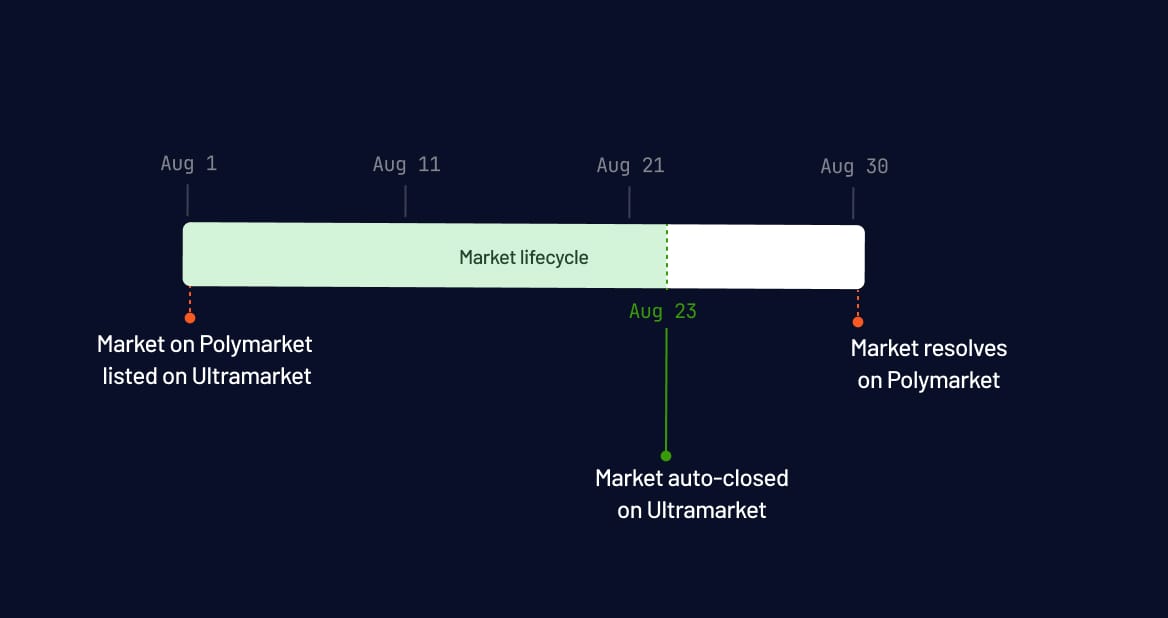

Every position on Ultramarkets auto-closes days or even weeks before the underlying event resolves. We currently close our markets 7–10 days before the corresponding Polymarket expiration. A Fed rate decision market on Polymarket might resolve after the April 28–29 FOMC meeting. On Ultramarkets, we're out by early April. An EPL season winner market might resolve in May on Polymarket. We're out by late March.

We call this temporal arbitrage — trading the probability volatility leading up to events, then exiting while the market is still functioning, where shares are priced between 0 and 1, order books have depth, and liquidation engines can do their job.

Why close 7–10 days out and not closer? Because closing 24 hours before would force us to unwind positions in exactly the window where liquidity is thinnest and volatility is highest — a recipe for bad debt. As our liquidation engine matures, we'll tighten this window. But conservatism is the right starting position for now.

Here's the thing though: temporal arbitrage only works if we can actually exit cleanly. If a market's order book is too thin to absorb our position, or if the event could resolve unexpectedly before our close window, the mechanism breaks.

This is why market listing is the most important risk decision we make. And it's why we formalize that decision as a Market Listing Proposal (MLP).

What Is an MLP?

An MLP — Market Listing Proposal — is the internal document we draft before any market goes live on Ultramarkets. Each one is a formal evaluation of whether a specific market or market category belongs on our platform, and if so, with what parameters. Below is a snippet of our MLP database 👀

Think of it like a collateral onboarding proposal at MakerDAO, or a new asset listing at Aave. The protocol's safety depends on getting these right, so we don't treat them casually.

Every MLP answers the same core question: can the vault safely exit this market before gap risk arrives?

To answer that, we evaluate markets across risk dimensions and operational criteria.

Risk as a Function of Time and Truth

Our risk framework is built on one principle: risk in prediction markets is a function of two variables — time and truth.

Time is the intuitive one. As a market approaches its resolution date, probability gets jittery. Small news items trigger bigger swings. Liquidity thins out as participants close positions. A position opened six months before an election carries fundamentally different risk than the same position opened six days before the vote. We can model the time dimension, plan around it, and build margin curves that account for it.

Truth is the harder one. Some events don't wait for their calendar date. New information surfaces — a leaked document, a surprise announcement, a geopolitical flashpoint — and the probability snaps toward 0 or 1 immediately, regardless of the scheduled resolution. Markets tied to whether a head of state makes a specific policy move, or Epstein file releases, or military escalations. The truth dimension creates unpredictable gaps that no forced-close schedule can fully protect against.

Both dimensions matter for every MLP. A market where the time dimension is well-behaved (clear resolution date, smooth probability path) but the truth dimension is wild (could resolve on a surprise announcement at any moment) is still dangerous. The inverse is also true.

If we can't confidently schedule an exit window where the market is still trading probabilities — not resolved truths — it doesn't get an MLP.

The Base Criteria Behind Every MLP

Beyond the time-truth analysis, every MLP evaluates these operational criteria:

Liquidity depth. Can the order book absorb our maximum position exit without slippage exceeding the margin buffer? We quantify this as the Market Depth Ratio — our maximum position size divided by average daily volume. If we'd move the price more than the trader's margin covers, the leverage is too high for that market.

Resolution certainty. Does this market have a known, fixed resolution date? Can that date change? Is the resolution source authoritative and unambiguous? Elections have certification dates. FOMC meetings are pre-scheduled. Markets where the date could shift, or the source is subjective, get lower leverage and wider forced-close buffers.

Truth stability. Is this a market where new information could cause an abrupt probability gap before our close window? Political events tied to a single individual's decisions, geopolitical flashpoints, breaking-news-dependent markets — these carry high truth-dimension risk. Some can still be listed with constraints. Others can't.

These criteria, evaluated through the time-truth lens, produce the MLP's recommendation: list or don't list, and if listed, with what leverage cap, position limits, and forced-close schedule.

What This Looks Like in Practice

Our Market Listing Framework defines three conceptual tiers — Institutional Grade (up to 10x), Retail Grade (up to 5x), and Experimental (up to 2x). But the tiers are a mental model. What actually governs trading is the per-market calibration that comes out of each MLP.

Across our active markets, leverage ranges continuously: 10x on a deeply liquid election market, 8x on the Fed rate decision or a Brazilian presidential race, 7x on La Liga title markets, 5x on F1 championships or the French presidential election, 3x on an NBA Rookie of the Year, 2x on lower-liquidity markets like the Serie A or certain crypto FDV predictions.

Position limits follow the same logic. Max trade amounts range from $1,000 to $10,000 per position. Trader-level OI caps range from $1,000 to $10,000. Aggregate market exposure caps range from $10,000 to $75,000. These reflect the vault's current TVL — during Genesis Season, they're conservative by design. As vault capital scales, the limits scale with it.

Today, the MLP process is manual — each proposal is drafted by the Ultramarkets Team and calibrated against live Polymarket data. That's intentional. The automated version is the target architecture. The manual version is the right approach when you're validating a risk model with real capital.

What Doesn't Get an MLP

Some markets are structurally incompatible with margin lending. No parameter adjustment makes them safe.

Markets that resolve on individual decisions. If resolution depends on whether a specific person chooses to do something — resign, acquire, announce — you cannot schedule a forced-close window against human free will. The event could gap toward resolution at any moment. Our temporal arbitrage only works when we can predict the timing of the gap and exit before it.

Markets with ambiguous resolution terms. When the ZachXBT identity market went viral and every platform spun up their own version, we chose not to list it. The resolution terms weren't defined well enough for us to confidently schedule close-out mechanics. Instead of treating it as a missed marketing opportunity, we explained publicly why we made that call. The credibility from saying "no" to a viral market is worth more than the volume from saying "yes" and getting burned.

NEW: Major investigation dropping February 26 on one of crypto’s most profitable businesses where multiple employees abused internal data to insider trade over a prolonged period of time. pic.twitter.com/Losou2CZ2N

— ZachXBT (@zachxbt) February 23, 2026

And then there's a third category — markets that fall in gray zones, where the risk is manageable but the mechanism needs to be different from a standard MLP. Live sports matches where volatility spikes in minutes. Markets driven by a single individual's social media activity, where truth is unstable by nature. Experimental formats where we're designing new resolution mechanics in real time.

These aren't markets we reject outright. They're markets that require a fundamentally different approach to listing. We've been running experiments in exactly these categories in our private beta — some went smoothly, others taught us lessons — and we'll break down what we learned in the next two parts of this series. Like really soon 👀

Why MLP Matters

If you're a trader, the MLP is the reason you can access up to 10x leverage on a prediction market without worrying about the protocol blowing up underneath you. Every market on Ultramarkets has been evaluated for whether the vault can exit safely if things go wrong. The leverage cap, the position limits, the forced-close schedule — none of it is arbitrary. It's calibrated to the specific liquidity and risk profile of that market.

If you intend to LP in the vault once it goes public, the MLP process is your primary protection. Your capital isn't being deployed against every viral Polymarket market that trends on CT. It's deployed against markets where we've done the work to ensure execution risk is bounded. The vault doesn't take directional exposure — it takes execution risk — and the MLP is how we keep that risk within the margin buffer.

And if you're watching the prediction market space more broadly: every new venue that launches — Kalshi, Opinion Labs, whatever comes next — is a potential source of MLP-eligible markets. The protocol is venue-agnostic by design. The MLP framework is what makes that possible without the vault becoming a directional bet on every event in the world.

Next up: How we approached listing a market driven entirely by one person's behavior, and what happens when truth is unstable by design.

Comments ()